- Cap rates held steady during 1H24, with significant variations across different property types.

- Most respondents believe cap rates peaked, reflecting improved sentiment driven by economic factors.

- Industrial cap rates fell, while office yields kept rising, showing sector-specific reactions to market conditions.

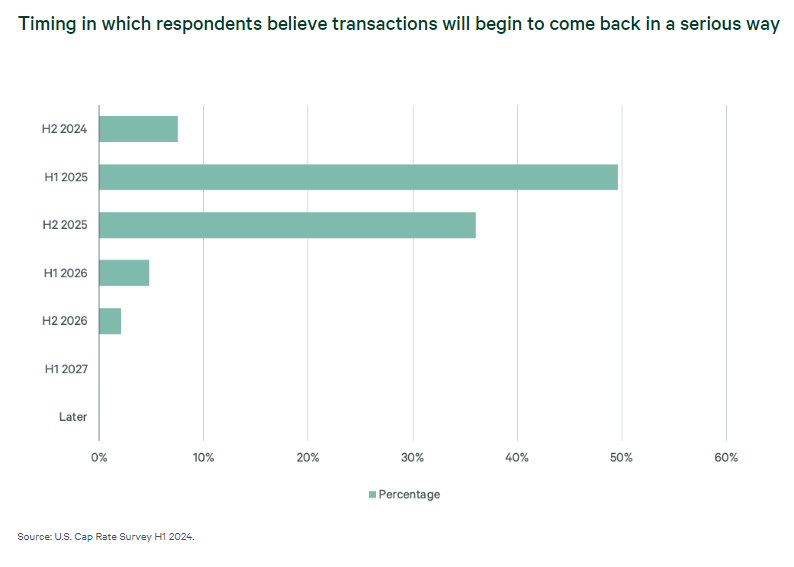

- Uncertainty around values and persistent inflation pushed expectations for sales volume recovery to 2025.

CBRE’s H1 2024 Cap Rate Survey, informed by deals from the first five months of 2024, captured 3.6K cap rate estimates across more than 50 geographic markets, revealing key trends and investor sentiments. Here’s what they found.

Holding Steady

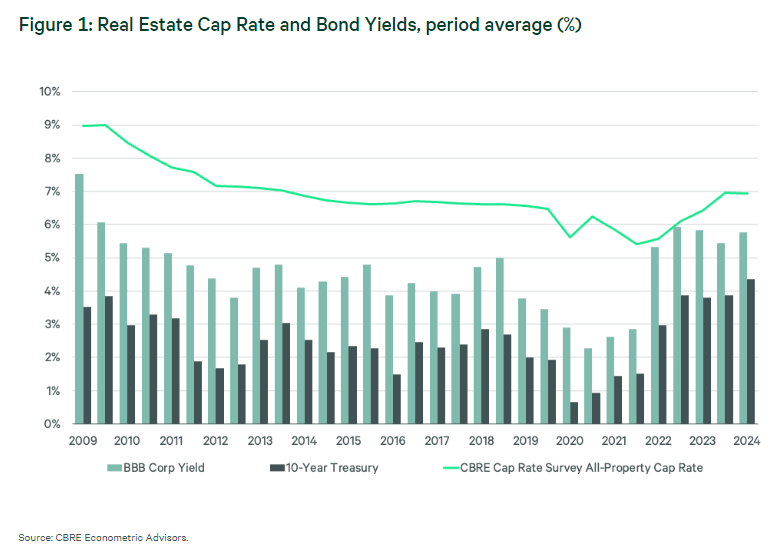

Despite volatile Treasury yields, which peaked at 4.7% in April before settling at 4.2% by June, the average survey cap rate remained stable. However, there were varied reactions across property types (e.g., industrial cap rates fell as office yields rose).

The survey reveals a shift in sentiment, with the majority of respondents thinking cap rates have peaked. The shift is attributed to less hawkish signals from the Federal Reserve and falling bond yields since October 2023.

Office Affairs

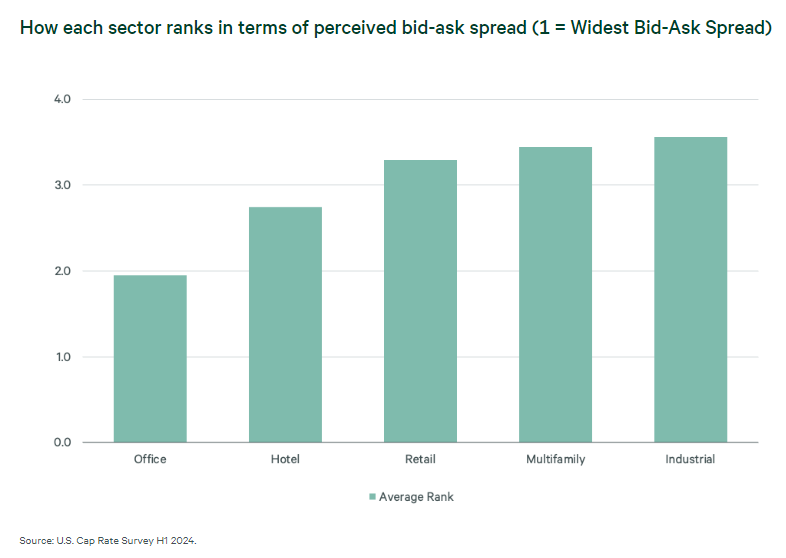

Notably, the office sector showed the highest expectation for more devaluations due to ongoing market uncertainties, as well as the widest bid-ask spreads.

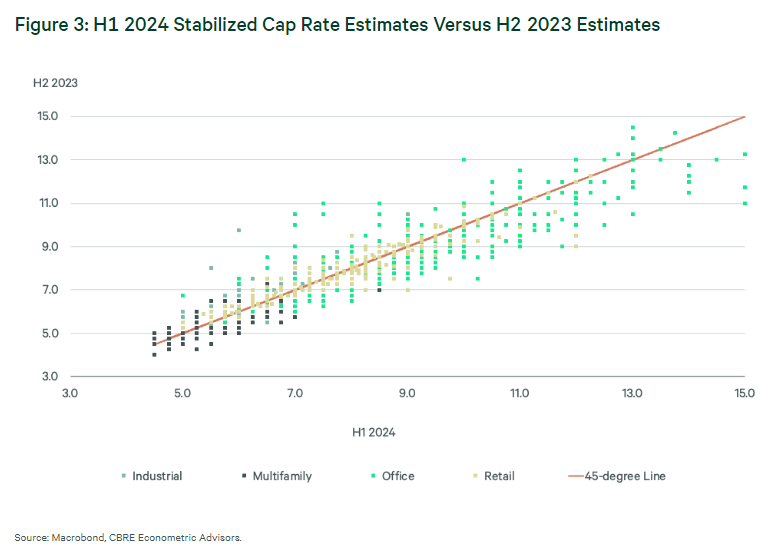

Comparing 1H24 stabilized cap rate estimates with 2H23, office properties saw the most yield expansion, with cap rates increasing by around 40 bps. The risk premium for Class A offices widened, with cap rates exceeding 8%, while Class C spaces faced distressed pricing, averaging the low teens.

Survey respondents highlighted capital markets and valuation metrics as the most challenging to estimate due to widespread price instability. Persistent inflation and high interest rates have delayed sales recovery, now anticipated to begin only in 2025.

Bigger Picture

- Industrial: Cap rates fell, driven by strong fundamentals and investor demand.

- Multifamily: Perceived bid-ask spreads are high, and few respondents expect yields in 2H24 will go up significantly.

- Office: Yield expansion continued, with significant disparities between Class A and Class C prices.

- Retail: This sector saw the highest YoY drop in the percentage of respondents who believe yields in 2H24 will go up significantly.

Hotels: Sentiment varied, with more respondents expecting cap rates to go up in the near term.