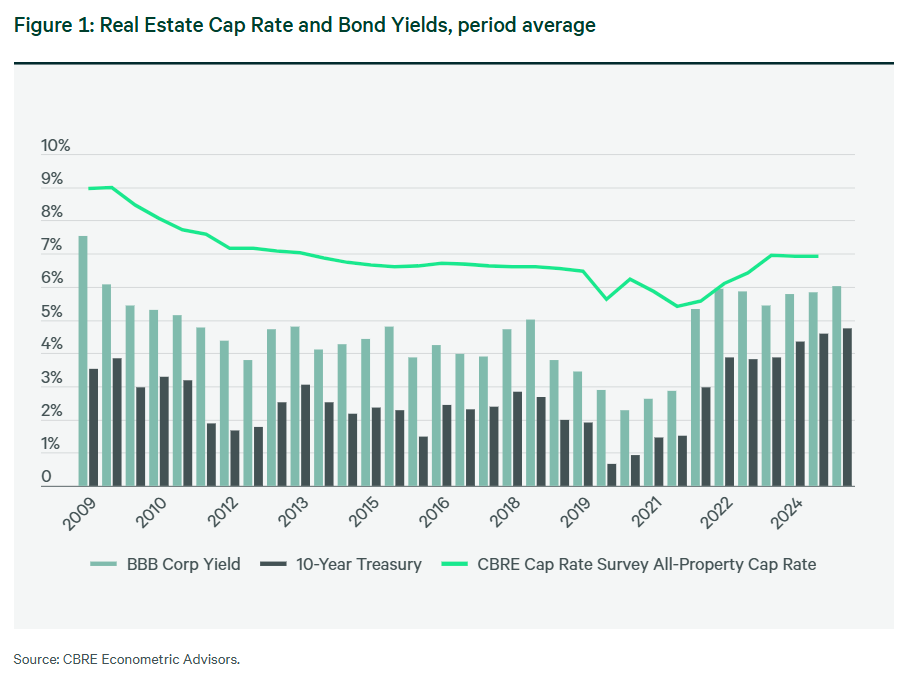

- US cap rates remained stable in 2H24, with variations. Industrial and multifamily cap rates compressed, while office cap rates rose due to distress.

- The 10-Year Treasury yield fluctuated but ended the year at 3.6% before rebounding in Q4, contributing to market uncertainty.

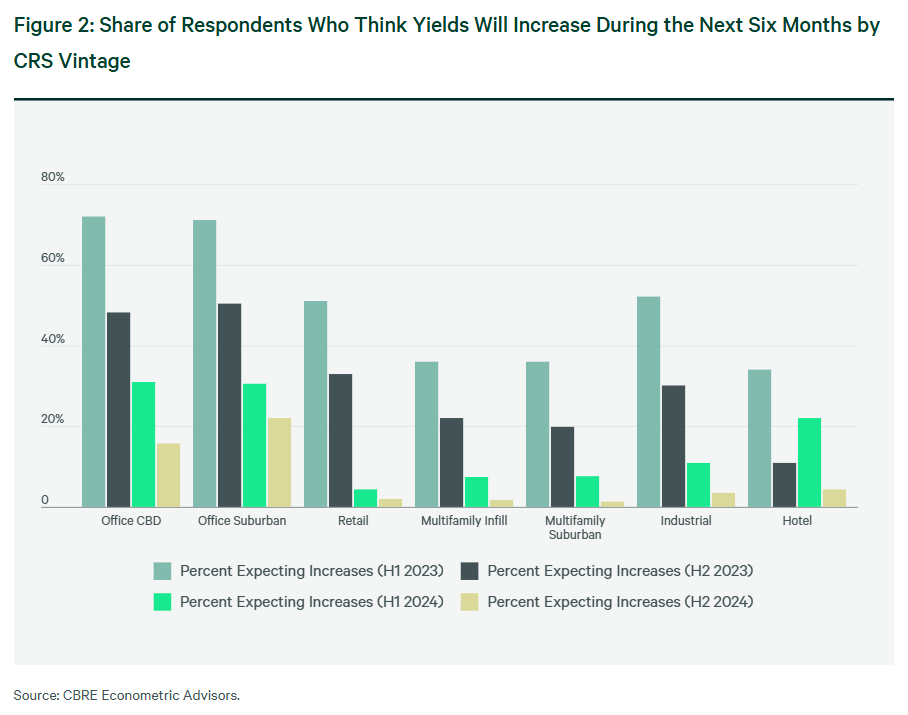

- Investor sentiment improved in H2, with most respondents believing cap rates have peaked, though office properties remain an outlier.

- Sales volume was up 9% in 2024 after a sharp 51% drop in 2023, and further growth is expected this year.

CBRE’s H2 2024 Cap Rate Survey (CRS) suggests that capitalization rates have mostly stabilized across the commercial real estate market. This follows a post-pandemic period of significant repricing in response to higher interest rates and economic uncertainty.

Survey Says…

The survey, which compiles 3.6K cap rate estimates across 50+ major markets, highlights several divergences in asset class performance.

Industrial and multifamily properties have seen cap rate compression, driven by stronger net operating income (NOI) growth expectations. Conversely, office cap rates have continued to rise, particularly for Class B and C assets, where uncertainty remains high.

Office Under Pressure

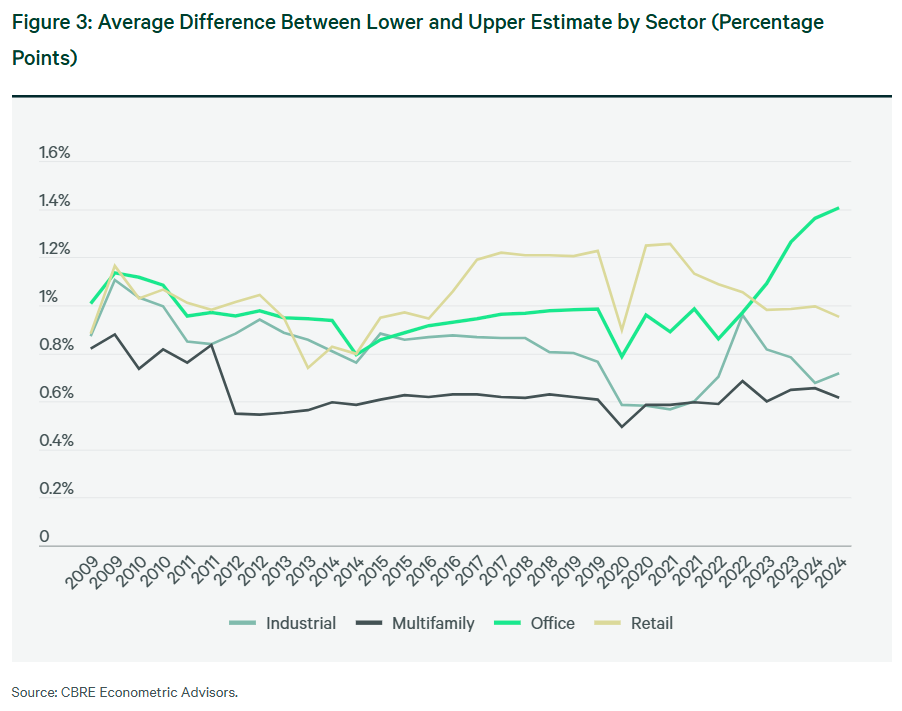

The office sector continues to be the most distressed segment, with cap rates widening further in H2. Stabilized Class A office cap rates now exceed 8%, while Class C office cap rates have reached the low teens, reflecting increased uncertainty.

The spread between upper and lower cap rate estimates has also widened, particularly in the commodity office segment, underscoring pricing challenges.

Prime office properties in key gateway cities are showing signs of recovery, benefiting from improving leasing activity. However, suburban office markets face more challenges, with weaker fundamentals leading to wider risk premiums. This tale of two office markets is expected to continue.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Rate Expectations

Treasurys saw substantial volatility throughout 2024, with the 10-Year Treasury yield peaking at 4.7% in April before falling to 3.6% in September. However, Q4 saw a reversal as the Federal Reserve signaled fewer rate cuts than anticipated, pushing yields back up.

Despite these fluctuations, cap rates across most cre sectors remained steady, reflecting a market that has largely adjusted to higher borrowing costs.

Optimistic Overall

Investor sentiment has certainly improved, with most survey respondents indicating they believe cap rates have already peaked. The share of investors expecting even higher cap rates has declined in each of the past three surveys.

After a steep 51% drop in investment sales volume back in 2023, the market saw a modest 9% increase in volume last year. While still below historical levels, this signals a potential turning point, with investors adjusting to the new interest rate environment.

Looking Ahead

As the market moves into 2025, investors will continue to monitor economic conditions, Fed policy, and bond market trends.

While cap rates appear to have stabilized for most asset classes, the office sector remains volatile, and the pace of transaction volume recovery will depend on broader macroeconomic factors.

CBRE anticipates transaction volumes to pick up more in 2025 as confidence continues to improve. The next Cap Rate Survey will be released in mid-2025 and should provide further insights into evolving investor sentiments and market trends.