- The potential slowdown in new multifamily supply after 2025 is positive for rent growth, given concerns surrounding distressed deals and defaults.

- Asset valuations are heavily influenced by the interest rate environment, presenting buying chances with relative value attractiveness.

- Potentially prolonged deleveraging could lead to long-term gains within 2 years.

Rising interest rates are hitting U.S. multifamily hard, according to KKR. Debt levels are higher than ever relative to equity, the looming loan maturity wall is coming fast, and an influx of new supply will hit the market over the next 2 years.

Different From Office

This all seems to indicate that multifamily is heading in the same direction as office—down a road of distressed deals and mounting defaults. However, unlike the office sector, the current obstacles in U.S. multifamily housing appear to be cyclical rather than lasting.

And even in the current downtrend, there’s an opportunity for high-quality properties at attractive prices amid upcoming market shifts. Experts are anticipating lower post-2025 supply, offering hope for recovering rent growth thanks to a combination of housing scarcity and discouraging new construction economics.

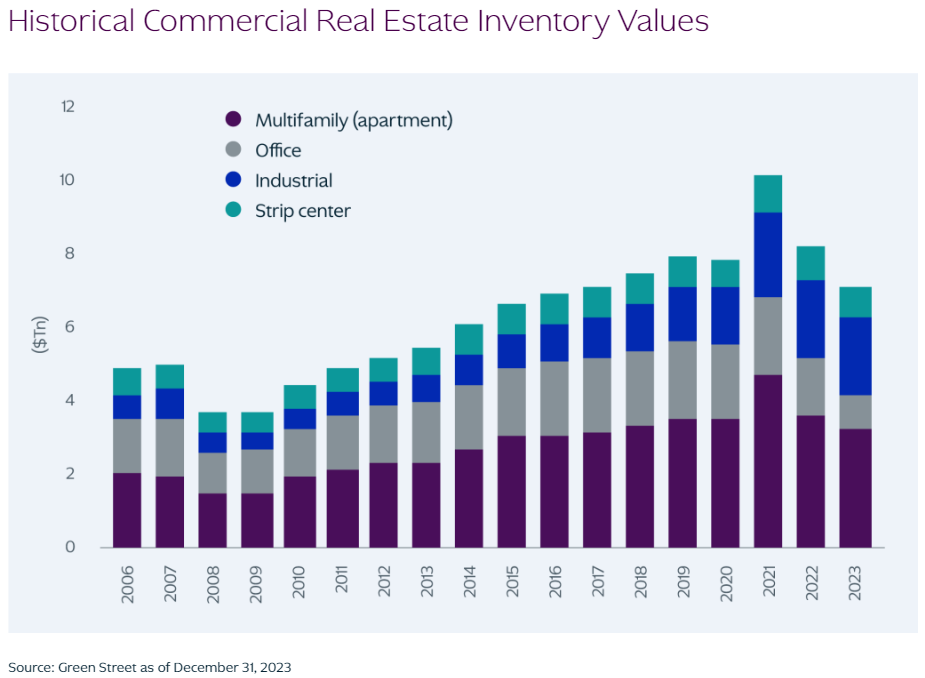

Emerging Valuations

Aside from the obvious decline in office inventory, multifamily values peaked in 2021 and have since slipped back down to 2017–2018 levels. Meanwhile, industrial values have enjoyed a three-year tear, shrugging off the post-pandemic slump that’s impacted other cre sectors. Strip center values have also held up well and are still close to pre-pandemic norms.

While most sectors are heavily correlated with interest rate dynamics, the U.S. and European office sectors are interesting outliers. They have primarily fallen due to emerging worldwide remote work trends. Understanding where these asset valuations become attractive investments in the current asset repricing environment is paramount.

What’s Next?

U.S. multifamily projects have historically exhibited high leverage as well as consistent performance through economic cycles. Despite a projected multiyear deleveraging cycle, multifamily owners who can hold steady and weather the storm stand to profit from “sustained structural demand” and a supply shortage expected to arrive by 2026.

Read More

This is just the tip of the iceberg. To read the rest of KKR’s April 2024 Real Estate Market Review, click here.