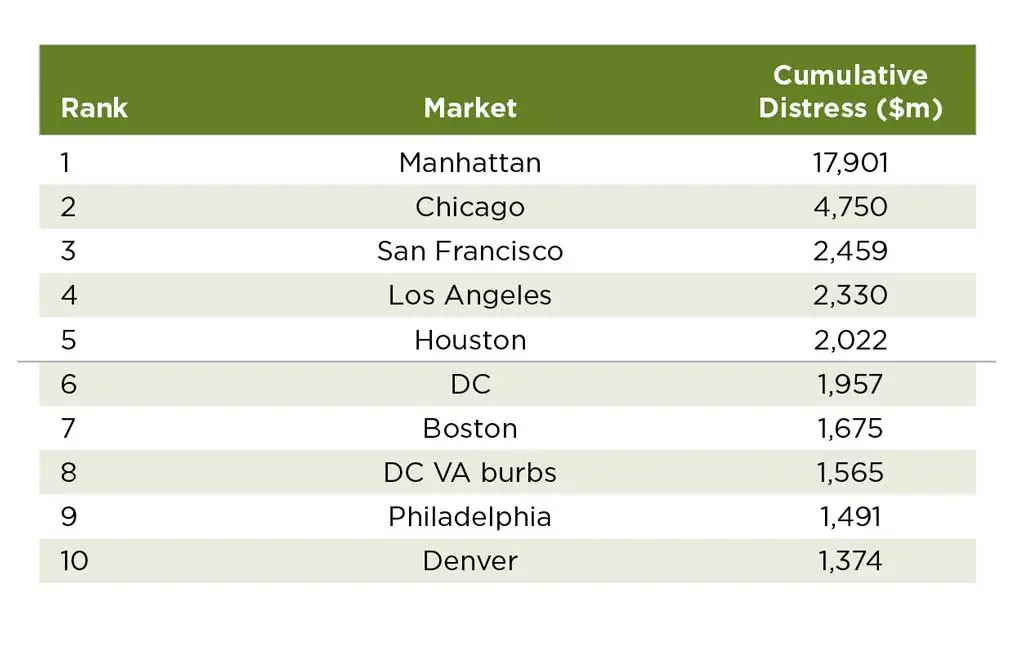

- US office distress surged to $51.6B in Q4, with another $74.7B at risk, per MSCI Real Assets.

- Urban office markets are under pressure as hybrid work fuels record-high vacancies.

- Class A properties remain resilient, while Class B and C offices are struggling to stay relevant.

- Office conversions are complex but could revitalize urban cores with the right incentives.

- Investors with fresh capital may benefit from lower-cost acquisitions and repositioning.

US office distress hit $51.6B in Q4, with another $74.7B at risk, according to Urban Land. While challenges persist, however, lower office valuations could unlock major opportunities.

Office Distress Deepens

Despite improving return-to-office trends, the entire US office sector is still dealing with high distress levels.

MSCI Real Assets reported that office accounts for nearly 50% of outstanding distress across CRE, totaling $51.6B by the end of 2024. Additionally, $74.7B in office properties are classified as “potential” distress.

Urban centers — traditionally driven by office activity — face major headwinds. Hybrid work remains the norm, with many employees only in the office 2–3 days per week. This has led to record-high vacancies, particularly in nonprime buildings.

Experts suggest that urban offices, especially those not considered premium, may need to undergo major transformations to remain viable.

Winners And Losers

While demand for high-end Class A offices in vibrant mixed-use districts remains strong, lower-tier Class B and C properties are struggling. Many office owners with distressed assets are negotiating with lenders, leading to potential sales at significant discounts.

Jim Costello, chief economist at MSCI Real Assets, notes that deeply discounted office assets could become viable again, as buyers can lease space at lower rates while still turning a profit.

However, today’s distress differs from the post-GFC era, when overleveraged assets drove defaults. Shifting tenant demand and structural changes in office utilization are the main culprits. As a result, traditional distress investment strategies may not yield the same returns as they did in past cycles.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Reinventing Urban Cores

The potential for conversion of underutilized office properties is a hot topic, but experts caution that only 20–30% of existing urban offices are physically and financially feasible for conversion.

Cities are also facing revenue pressures as declining office values erode key tax bases, making a strategic repositioning of these assets even more mission-critical.

Of course, everything’s a matter of perspective. Rebecca Rockey, deputy chief economist at Cushman & Wakefield, sees a “once-in-a-generation opportunity” for cities to rethink land use and real estate strategy.

Some downtowns may transition to more mixed-use environments, incorporating residential, hospitality, and entertainment to drive foot traffic beyond 9-to-5 office hours.

Overall Outlook

Market observers agree that office distress is not a death sentence for urban centers but rather a catalyst for transformation—provided that policymakers and investors move decisively to reshape the future of office real estate.

With over 10% of office CMBS loans currently delinquent, per Trepp, more distress is expected in 2025. However, well-capitalized investors and developers who can navigate the complexities of conversions, renovations, and strategic acquisitions could benefit from this reset.