DC Retains Top Spot for US Renters in 2025

Washington, DC, remains the most sought-after US rental market in 2025, with 7% more favorited listings.

Jordan B.

March 04, 2025

Together with

Good morning. Washington, DC, remains the most sought-after US rental market to kick off 2025, with 7% more favorited listings, while Southern cities and smaller, affordable markets like Philadelphia also gained traction.

Today’s issue is brought to you by WareSpace, the next-gen of small bay industrial.

Market Snapshot

|

|

||||

|

|

*Data as of 03/03/2024 market close.

Leading The Nation

Washington, DC Retains Top Spot for Renters in 2025

Washington, DC, continues to lead as the most sought-after city for US renters, according to RentCafe’s January data, with 7% more favorited listings.

Capital on top: According to RentCafe data, DC solidified its position as the most popular US city for renters as we enter 2025. With a 7% jump in favorited listings in January, the nation’s capital continues to attract a steady stream of renters, drawn by its combo of top-tier healthcare, economic opportunities, and a vibrant cultural scene.

The South rises: While DC holds firm at the top, nearly half of the cities in RentCafe’s top 30 are located in the South. The region's appeal is undeniable: It offers affordable living combined with robust job markets, a trend that seems to be accelerating.

Standout cities: St. Paul, MN, saw a dramatic surge in renter interest, with a staggering 114% more favorited listings than last January, part of a growing trend toward smaller, more affordable cities. Meanwhile, Cincinnati shot up 10 spots since November, driven by its affordable cost of living and expanding job market.

Brotherly love: Philadelphia, which ranks fifth, also saw more renter interest. Pageviews rose 26%, and saved listings soared 94%, signaling Philly’s affordable urban lifestyle continues to attract renters. Despite a slight dip in saved searches—indicating renters are moving quickly to secure leases—Philly’s robust demand shows no signs of waning.

Near the top 10: This year, Las Vegas made a dramatic leap, jumping 69 spots to land at No. 11, indicating a sharp rise in renter interest. Additionally, seven new cities cracked the top 30, many located in the South, revealing the region’s growing allure.

➥ THE TAKEAWAY

Zooming out: The US rental market is shifting, with DC, Atlanta, and Philadelphia holding steady, while cities like St. Paul and Cincinnati reflect changing renter preferences. As cities like Las Vegas and St. Paul gain traction, traditional hubs like Los Angeles and New York face new challenges in an increasingly competitive market.

TOGETHER WITH WARESPACE

We’re deploying $500M to acquire industrial properties

WareSpace is the next-gen of small bay industrial.

Think micro-bay spaces built for small businesses—with one simple monthly payment that covers everything, including equipment, racking, shared kitchens, conference rooms, etc.—the kind of features small businesses actually want.

With $500M in capital ready to deploy, WareSpace is actively acquiring industrial, flex, office, and big box retail (50K–250K SF).

We prefer immediate or near-term vacancies, including Class A–C properties with loading docks or drive-ins. Transitional assets needing capex are welcome.

All-cash closings with substantial buyer-side commissions.

Have a deal? Send it to VP of Acquisitions, Jeff Jenkins at [email protected].

*Disclosure: This is a paid advertisement. Please read the disclosure at the bottom of the newsletter.

✍️ Editor’s Picks

-

Find the right tools: Compare features and pricing on top CRE software and products to streamline operations and boost efficiency.

-

Positive prices: US CRE prices rose 0.3% YoY in January, with retail leading at 5%, while industrial grew 3.4%, apartments dropped 1.6%, and major metros saw declines.

-

More completions: Despite a construction slowdown, the US multifamily sector is set to deliver the second-highest new supply since 2008, led by affordable housing and single-family rentals.

-

Rejected bid: Howard Hughes (HHH) rejected Bill Ackman’s $90 per share takeover offer but agreed to continue talks under a standstill agreement until March 13 to explore potential alternatives.

🏘️ MULTIFAMILY

-

Zoning reform: Cambridge’s new zoning law permits up to 6-story buildings in residential areas, potentially adding 4.88K units and setting a new standard for housing development in the city.

-

Local bank distress: US community bank multifamily loans are seeing rising delinquencies, with over $6B in loans late and realized losses hitting $504M, signaling mounting distress.

-

Refinancing finance: Apollo Global Management (APO) provided a $275M loan to refinance a luxury apartment complex at 63-67 Wall St. in NYC’s financial district.

-

Sunbelt strength: RMR Residential (RMR) sees strong demand in Sunbelt markets like Dallas, Denver, and Florida, using data to explore value-add acquisitions amid a rent growth slowdown.

-

Union-built housing: Former Governor Andrew Cuomo, endorsed by NYC construction unions, vows to build thousands of affordable housing units with union labor if elected mayor.

🏭 Industrial

-

Data center boost: Mansfield, Red Oak, and Garland, TX, are leveraging data center investments to boost economies and beautify spaces, with billions fueling local economies.

-

Supply surge: Data center supply surged 34% YoY, with demand driven by AI and cloud services, leading to record-low vacancies and rising rents in key markets like Atlanta and Northern Virginia.

-

Emissions concerns: Higher demand for faster deliveries has led to more truck emissions, with NY and CA proposing regulations for air pollution and health impacts from large distribution centers.

-

Done deal: Ares Management’s (ARES) acquisition of GLP’s international business, excluding China, creates a top-three global industrial owner, now holding $115B in real assets.

🏬 RETAIL

-

Grocery wars: Target (TGT) purchased a $231M Denver distribution center, enhancing its logistics network ahead of announcing its growth strategy amid mounting competition.

-

Tight market: Despite a large construction pipeline, Houston’s retail market remains fragmented, with limited availability of quality space and slowing rent growth in some areas.

🏢 OFFICE

-

Tech exodus: Miami’s tech scene, once booming with VCs, has slowed down as many tech firms and founders return to the Bay Area, leaving behind shrinking office leases and unmet talent needs.

-

Manhattan interest: In 2025, NYC’s prime office buildings are seeing renewed investor interest, driven by strong demand and record-high rents, while less desirable properties remain sidelined.

-

Eyeing trophies: With corporate demand rising, developers like SL Green (SLG), RXR Realty (RXR), and Vornado (VNO) are ramping up plans for high-end Manhattan office towers.

-

Cincinnati leads: Greater Cincinnati tops US cities for office-to-residential conversions per capita, though there's still a big supply of office space left for potential transformation.

🏨 HOSPITALITY

-

Florida weakness: DiamondRock’s Florida hotels saw RevPAR fall 5.8% in Q4, citing high inflation and post-pandemic problems, but a 2025 recovery is expected despite uncertainties.

-

Third-party shift: Davidson Hospitality sees opportunities as more high-end hotels move to third-party management, with owners seeking experienced operators beyond traditional brand control.

-

Bigger bunkhouse: Fresh off Hyatt’s (H) $335M acquisition, Bunkhouse Hotels debuts two new Houston properties, reinforcing its community-driven approach to hotels.

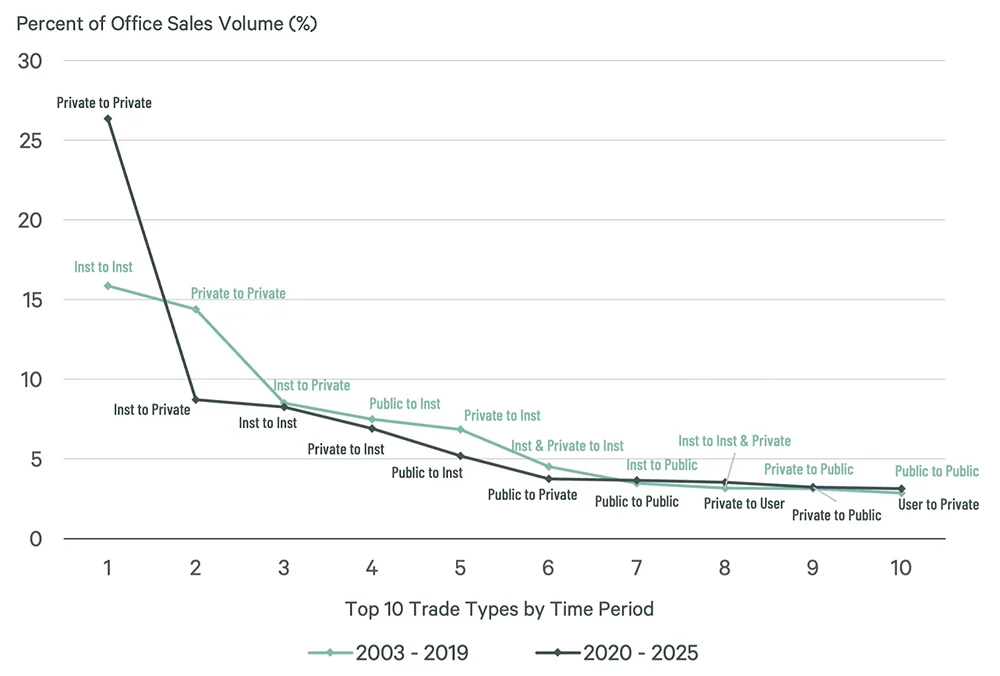

📈 CHART OF THE DAY

According to CBRE, the composition of office sales has shifted in recent years, with institutional investors playing a larger role while private deals have declined.

From 2003–2019, "Private to Private" transactions dominated office sales, accounting for over 25% of the volume, while "Inst to Inst" followed with about 15%.

However, from 2020–2025, these patterns shifted, with "Inst to Inst" and "Inst to Private" more prevalent. "Private to Private" deals slipped, revealing a broader trend toward institutional office deals.

You currently have 0 referrals, only 1 away from receiving B.O.T.N Multifamily Deal Screener .

What did you think of today's newsletter? |