Fitch: US Apartment Defaults Will 2x in 2024

CRE prices are converging to the downside across sectors—industrial being the only exception.

Jordan B. & Han-Gwon Lung

February 01, 2024

Together with

Good morning. U.S. apartment defaults may double this year with increased supply, cost challenges, and loan issues. Meanwhile, CRE prices fell across just about every sector in Q4 23, except industrial, thanks to higher consumer spending.

Today’s issue is brought to you by Greysteel.

Market Snapshot

|

|

||||

|

|

*Data as of 1/31/2024 market close.

ON THE RISE

Fitch: US Apartment Defaults to Double This Year

More apartments are expected to face default in 2024, Fitch says. (PHOTO: PEXELS)

Fitch Ratings is predicting a surge in loan defaults in the U.S. multifamily market. According to Multifamily Dive, apartment delinquencies for CMBS loans could reach $1.3B this year, surpassing losses during the height of the pandemic.

Record supply, strain: Multifamily is facing headwinds due to record new supply, with 900K units under construction and over 440K set to be delivered this year, per CBRE. This influx of inventory is dampening revenue growth and bumping up expenses, leading to less cash flow and more apartment owners struggling to meet their loan obligations.

Rising delinquencies: The delinquency rate on multifamily CMBS loans has already risen, climbing from 1.6% six months prior to 2.6% in December, according to Trepp. As the strain on apartment owners continues, this rate is expected to further increase, highlighting the mounting challenges facing the sector.

Ticking time bomb: The next five years pose significant challenges when it comes to maturities. Over $31.2B in conduit and agency CMBS loans are set to mature this year, followed by $37.9B in 2025, compared to $26.5B from October 2022 to December 2023. Most maturing loans are in retail, office, and multifamily. While refinancing performed better than expected, rates fell over the past six months.

Ready to take it: Despite the looming loan maturities, some industry experts are not overly concerned. With historically low unemployment and continued job creation, the economy’s resilience should be able to soften the blow from maturities. More inviting interest rates can also ease refinancing. However, apartment owners may still need gap financing.

More gap financing? Around $1T in total multifamily debt is set to mature through 2028. As rates fall, there may be better opportunities to refinance by 2025. However, the need for owners to contribute funds for refinancing remains a possibility—especially if the Fed opts for more conservative adjustments.

Hope on the horizon: Despite difficulties, experts think relief may be around the corner. CBRE predicts developers will scale back on new projects. And the Fed is projected to make rate cuts later this year. This could pave the way for a strong recovery in both occupancy and rent growth. Experts anticipate 45% fewer starts this year compared to pre-pandemic levels—70% less than the 2022 peak.

➥ THE TAKEAWAY

Cautious optimism: While U.S. multifamily faces challenges, there are several potential signs of relief. CBRE experts predict fewer new developments and rate cuts, which could lead to improved occupancy and rent growth. As multifamily braces itself for billions in impending loan maturities, owners and operators need to adopt proactive refinancing, including potential gap financing requirements.

SPONSORED BY GREYSTEEL

With 45L and 179D energy efficiency tax incentives as high as $5,000 per unit and $5.00 per square foot, our clients average more than $150,000 in tax benefits.

These tax incentives are available not only for real estate investors, but also for commercial developers, single family home developers, manufactured home developers, REITs, and architects.

Greysteel Advisory’s expert team of tax professionals, attorneys, and engineers make the process of harnessing 45L and 179D energy efficiency tax incentives simple, fast, and profitable.

As deal flow has slowed and the industry is in a holding pattern waiting for interest rates to drop, now is the moment to capitalize on this opportunity.

Take the first step towards maximizing your ROI and see if your project qualifies for tax incentives today.

✍️ Editor’s Picks

-

Shaking things up: New supply impacts market equilibrium and asset performance even as construction costs surged during pandemic, according to Marcus & Millichap.

-

Raising the Bay: The U.S. Army Corp of Engineers proposes raising San Francisco’s bay shoreline by seven feet. That’ll be $14B, thanks.

-

Stepping up to the plate: The Baltimore Orioles were sold to David Rubenstein’s group for $1.73B, pending league approval; Rubenstein initially acquired 40%.

-

Viva Las Vegas: Of all major U.S. metros, Vegas CRE enjoyed the biggest boost in tourism with major events like Formula One and the Super Bowl driving revenue and development.

🏘️ MULTIFAMILY

-

Multifamily mixup: Investors remain frustrated as the anticipated wave of distressed multifamily properties fails to materialize, impacting trading activities.

-

Market mayhem: The 199-unit apartment building at 1411 S. Michigan Ave. in Chicago is facing an $80M foreclosure lawsuit, marking the city’s largest multifamily foreclosure since 2022.

-

Foreclosure frenzy: Greystar Real Estate Partners faces foreclosure on a Dallas apartment building after taking out a $127M mortgage in early 2022.

-

Next hotspot: A Blackstone (BX) subsidiary plans to build a 500-unit complex near the Domain in North Austin.

🏭 Industrial

-

Warehousing win: LBA Realty purchased two warehouses with 480KSF of space near O’Hare for $95M, doubling their 2019 investment of $83M.

-

Robot revolution: Lanier Investments secured a 5-year lease for a 60.3KSF warehouse in San Fernando Valley for robotics and AI-driven manufacturer Machina Labs.

-

Taking flight: AE Industrial Partners purchased a 2.3MSF industrial facility in Cherokee, AL for $190 Mto create an aerospace hub.

🏬 RETAIL

-

Retail redux: Lexington Partners plans to transform the Westbrook Outlets into a mixed-use campus with hotels, apartments, townhouses, and restaurants, costing $425M.

-

Manhattan-made: The Jackson Group buys a mixed-use building on Madison Avenue in NYC for $14.5M.

-

Retail rebirth: The so-called retail apocalypse never really happened, as the vacancy rate for shopping centers in the U.S. is currently at its lowest point in 15 years.

🏢 OFFICE

-

Rather embarrassing: Morgan Stanley (MS) just unloaded a downtown Chicago office building for 90% off what it originally paid, settling for just $16PSF.

-

Office blues: Office deal volume in 4Q23 dropped 66% below the average volume between 2015–2019. Not entirely surprising.

-

Data destination: CoStar plans to acquire Northern Virginia’s Central Place office tower and relocate its HQ from Downtown D.C.

-

Office boom: Denver leads its peer cities in the Western U.S. with 2.3MSF of office space under construction, but leasing activity remains uncertain.

-

Building collapse: The collapse of the Miami Beach office building deal puts Nightingale’s $82M payback to investors at risk.

ACROSS SECTORS

Office, Multifamily, and Retail Suffer From Falling Property Values Except for One Sector

CoStar Group’s industrial value indices show values rose both in the fourth quarter and for the year. (Getty Images)

CRE prices suffered a Q4 drop, with the exception of industrial real estate, which has benefited from increased consumer spending, according to a CoStar Group analysis.

Impact on institutional: Falling values for office, multifamily, and retail in Q4 were most significant among investment-grade properties, which are typically larger-sized real estate often purchased by institutional investors. The drop in values reflects the current economic conditions.

Industrial growth: Industrial property values have shown growth, as demand for warehouse space remains positive. Despite a slowdown in leasing activity in 2H23, early signs of stabilization and a recovery in tenant demand are emerging, setting the stage for potential growth in late 2024.

Office slump: The value-weighted office index saw a 26% plunge from its peak in 4Q21. The index also fell by 10.8% compared to 4Q22 and 1.9% compared to 3Q23. The equal-weighted office index saw milder declines but still shed 2.1% over the prior quarter, 2.7% over the prior year, and 6.9% compared to its peak in 2Q22.

Multifamily mood: The value-weighted multifamily index slipped by 0.3% in Q4 and suffered an 11.1% drop in the 12-month period ending December. Compared to its peak in 2Q22, the value-weighted index fell 18.3%. However, the equal-weighted multifamily index remained stable, with no change over the prior quarter and down just 0.5% YoY.

Rock-steady retail: The value-weighted retail index fell by 2.5% in Q4 compared to its peak in 3Q22, and slipped 0.5% YoY. Equal-weighted retail pricing also showed a decline, down 0.2% in Q4 compared to the prior quarter. However, the index gained 2% compared to 4Q22.

➥ THE TAKEAWAY

Commercial convergence: U.S. industrial property values, driven by increased consumer spending, have shown resilience while all other CRE sectors have seen decreases. While cap rate increases have paused for now, future capital flows into the sector may continue to contain any future increases indefinitely. Converging trends indicate that CRE values, particularly in smaller markets, may converge lower.

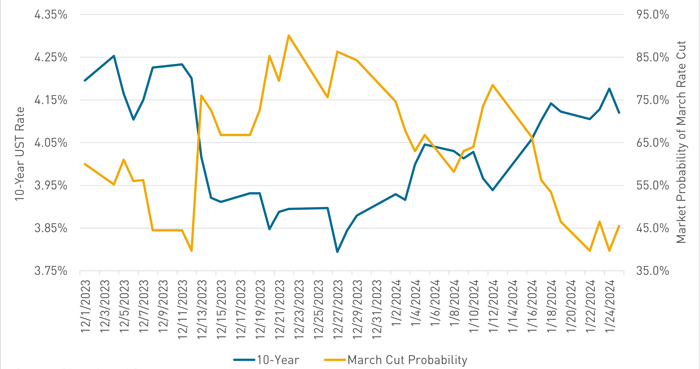

CHART OF THE DAY

IMAGE: BERKADIA

Last December, market optimism for a dovish Fed rate cut by March reached a peak 90% probability. But as the 10-Year Treasury rate continues to rise (tapping 4.15% last week), that optimism faded fast—now the market only thinks there’s a 45% chance of a Fed rate cut by March this year.

What did you think of today’s newsletter? |