Sharp Downturn in Multifamily Construction Starts

January saw a significant 36% drop in multifamily construction starts, marking the lowest level since the pandemic’s onset..

Jordan B. & Han-Gwon Lung

February 19, 2024

Together with

Good morning. January witnessed a notable decline in multifamily housing starts, overshadowing the slight recovery in single-family production. Meanwhile, Arbor Realty is starting to feel the strain from late mortgage payment pileups.

Today’s issue is brought to you by Greysteel.

Market Snapshot

|

|

||||

|

|

*Data as of 2/16/2024 market close.

-

JBG Smith (JBGS) cuts its dividend by 22.2% to 17.5 cents a share, aiming to enhance financial flexibility amid a core development focus.

-

CBRE Group (CBRE) saw a 30% decline in annual profit amid industry-wide reduced property demand, prompting a strategic shift towards more stable business areas.

MULTIFAMILY MAHEM

Multifamily Construction Starts Plunge Nearly 36% in January, Permits Rise

January saw a significant drop in multifamily construction starts, marking the lowest level since the pandemic’s onset.

By the numbers: According to Census Bureau figures released Friday, overall housing starts fell by 14.8% in January to a seasonally adjusted annual rate of 1.33 million units. This downturn was driven primarily by a 35.6% drop in multifamily sector starts, which plummeted to an annualized pace of 327,000 units. In contrast, single-family starts decreased by a modest 4.7% to 1 million units but showed a 22% increase from the previous year.

-

Regional trends: The Northeast, Midwest, South, and West experienced decreases in combined single-family and multifamily starts by 20.6%, 30%, 9.7%, and 15.7%, respectively. Permit data also reflects these regional disparities, with notable increases in the Northeast and Midwest but declines in the South and West.

-

Permits: Overall permits in January fell by 1.5% to a 1.47 million unit annualized rate. Single-family permits rose by 1.6%, reaching the highest level since May 2022, while multifamily permits declined by 7.9%, marking the lowest point since April 2020.

-

Construction: The number of apartments under construction has fallen below 1 million for the first time since May 2023, with further reductions anticipated. Conversely, the number of single-family homes under construction remained steady at 680,000, equaling the highest count since June 2023.

What they are saying: Andrew Foran, TD Bank Economist, notes that volatility is typical in the multifamily segment. He pointed out that the sharp decline was somewhat anticipated following a strong December performance, which was later revised upwards. However, he also acknowledges the challenges faced by the segment, including high financing costs, slowing rent price growth, and an accumulation of projects from recent years.

➥ THE TAKEAWAY

Looking ahead: There is optimism for a rebound, with the possibility of the Federal Reserve cutting interest rates in the first half of the year. The National Association of Home Builders reported a surge in confidence among single-family builders to an 18-month high in February. The survey also noted a decrease in builders reducing home prices and offering sales incentives.

SPONSORED BY GREYSTEEL

Maximize Your Returns With Greysteel Advisory’s Transformative Tax Strategies

With 45L and 179D energy efficiency tax incentives as high as $5,000 per unit and $5.00 per square foot, our clients average more than $150,000 in tax benefits. These tax incentives are available not only for real estate investors, but also for commercial developers, single family home developers, manufactured home developers, REITs, and architects.

Greysteel Advisory’s expert team of tax professionals, attorneys, and engineers make the process of harnessing 45L and 179D energy efficiency tax incentives simple, fast, and profitable.

As deal flow has slowed and the industry is in a holding pattern waiting for interest rates to drop, now is the moment to capitalize on this opportunity.

Take the first step towards maximizing your ROI and see if your project qualifies for tax incentives today.

✍️ Editor’s Picks

-

Tech return: After relocating during the pandemic, tech leaders and investors are returning to San Francisco, drawn by an AI boom and rich tech talent.

-

Regulators are right: Former Treasury Secretary Lawrence Summers emphasized the importance of regulatory focus on CRE risks, suggesting it should be a higher priority than boosting capital standards among large banks.

-

Tax tango: Chicago’s proposed real estate transfer tax could increase dramatically, with rates up to 3%, potentially impacting deal volume.

-

Credit concerns: Global fund managers are increasingly worried about a potential systemic credit event triggered by global distress signals in property markets.

-

Cushman in crisis: As Cushman & Wakefield (CWK) gears up for a challenging year, it grapples with a crisis of confidence amidst leadership instability, financial struggles, and mounting pressure from competitors and investors.

🏘️ MULTIFAMILY

-

Housing law rejected: Residents in Milton rejected a state-mandated zoning plan in a 5,115–4,346 vote, jeopardizing state funding and legal compliance.

-

Informative insights: National average rent remains steady, with varying growth and supply across regions, with high-growth markets in the West and Sun Belt.

-

Sheltering hope: The HUD’s 2023 report notes a 12% increase in homelessness with 650K people without housing; 991K new units are under construction.

-

Tax breaks: Governor Hochul introduced an alternative to the 421a tax break for 18 Gowanus projects that will revive 5,300 apartments.

🏭 Industrial

-

Warehouse shuffle: GLP Capital Partners sells a few Texas warehouses, like CentrePort 2 in Fort Worth and Northwest Logistics Center in Houston for a $49.2M loan.

-

Strategic takeover: Realterm acquired 3 truck terminals in Boston, Philadelphia, and Providence as part of Yellow Corp.’s bankruptcy, totaling 163 doors.

-

Logistics boom: Construction begins on the first phase of Park 4 Logistics Center in Plant City, FL, comprising four buildings totaling 860.12KSF.

🏬 RETAIL

-

Retail reality check: January retail and food service sales totaled $700.3B, down 0.8% from December 2023 but up 0.6% YoY.

-

Fulton fallout: Westfield Corp. plans to close Fulton Center early, disrupting leasing and development progress in Manhattan post-9/11.

-

Walmart wonders: In 2023, Walmart’s (WMT) total revenue rose 6.7% to $611.3B, which led to pay increases, stock split, and store remodels.

🏢 OFFICE

-

Podcast: For years, a crisis has been looming in US CRE. The Big Take podcast dives into why this crisis is coming to a head now and what it means for lenders and investors across the globe.

-

Tax break boost: Washington DC aims to boost office-to-residential conversions with a 20-year tax abatement, as 1MSF office space sits vacant.

-

Loan default chaos: Starwood Capital (STWD) and Artisan Ventures face foreclosure on a 257KSF office building in El Segundo due to an $84.8M default with MetLife (MET).

-

Recapitalizing: KBS couldn’t repay a $600M loan on six offices, mostly in Texas, although its loan was extended to August.

LENDING & INTEREST RATES

Rising Interest Rates Strain Arbor Realty’s Loan Repayments

Arbor Realty Trust (ABR), a beacon in the Sun Belt’s multifamily lending scene, is starting to feel the pinch from skyrocketing interest rates over the last two years.

What happened: Long Island-based Arbor Realty Trust became a significant lender in the Sunbelt region’s apartment market, helping drive a multifamily boom in 2021 and early 2022. However, the surge in interest rates that followed led to difficulties for borrowers with floating-rate debt to meet their loan obligations, which were often converted into bonds for investors.

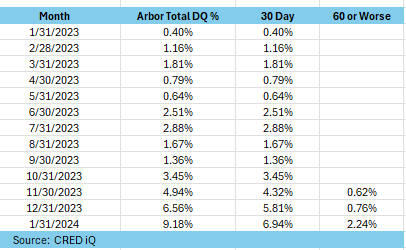

The strain: Data from CRED iQ shows that as of mid-January, a quarter of Arbor’s securitized debt witnessed late payments, with about 9% being 30 days or more overdue. Although most borrowers paid eventually, 5.8% of Arbor’s securitized debt payments remained overdue.

Arbor Realty Trust CLO Delinquency Rate – Source: CRED iQ

Earnings report: Arbor’s earnings report on Friday reveals a significant increase in nonperforming loans, rising to 16 from 12 in the previous quarter, with the value jumping from $150.5 million to $262.7 million. The company also ranks as the 17th most shorted stock, signaling investor concerns for future challenges.

“With today’s current interest rates, we will continue to chip away at converting the loans to the agencies,” said Arbor’s CEO Ivan Kaufman. “But if the 10-year [Treasury rate] goes below 4 percent again, it will become more meaningful and every quarter of a point drop in rates from here will be even more impactful.”

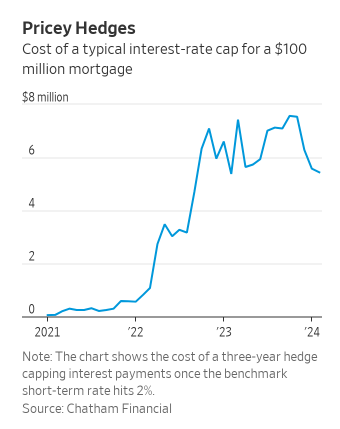

The silent killer: Arbor Realty confronts growing risks with borrower defaults and expiring interest rate hedges—65% of the 2021 caps have expired, and 92% will by year’s end. Its CLO loan income now covers only 60% of debt payments. Renewing these hedges has become difficult, with a three-year hedge for a $100 million mortgage jumping from $51,000 to $5.4 million.

➥ THE TAKEAWAY

A challenging cycle: Arbor Realty Trust CEO Kaufman remains optimistic about the demand for workforce housing, a key segment of their portfolio, despite vacancy challenges in the Sun Belt markets. He anticipates that the influx of workers from the Mexico border will positively affect vacancy rates. However, the company is preparing for ongoing difficulties by maintaining around $1B in cash to mitigate potential losses. This comes amid a trend where some borrowers are choosing to default first and negotiate later.

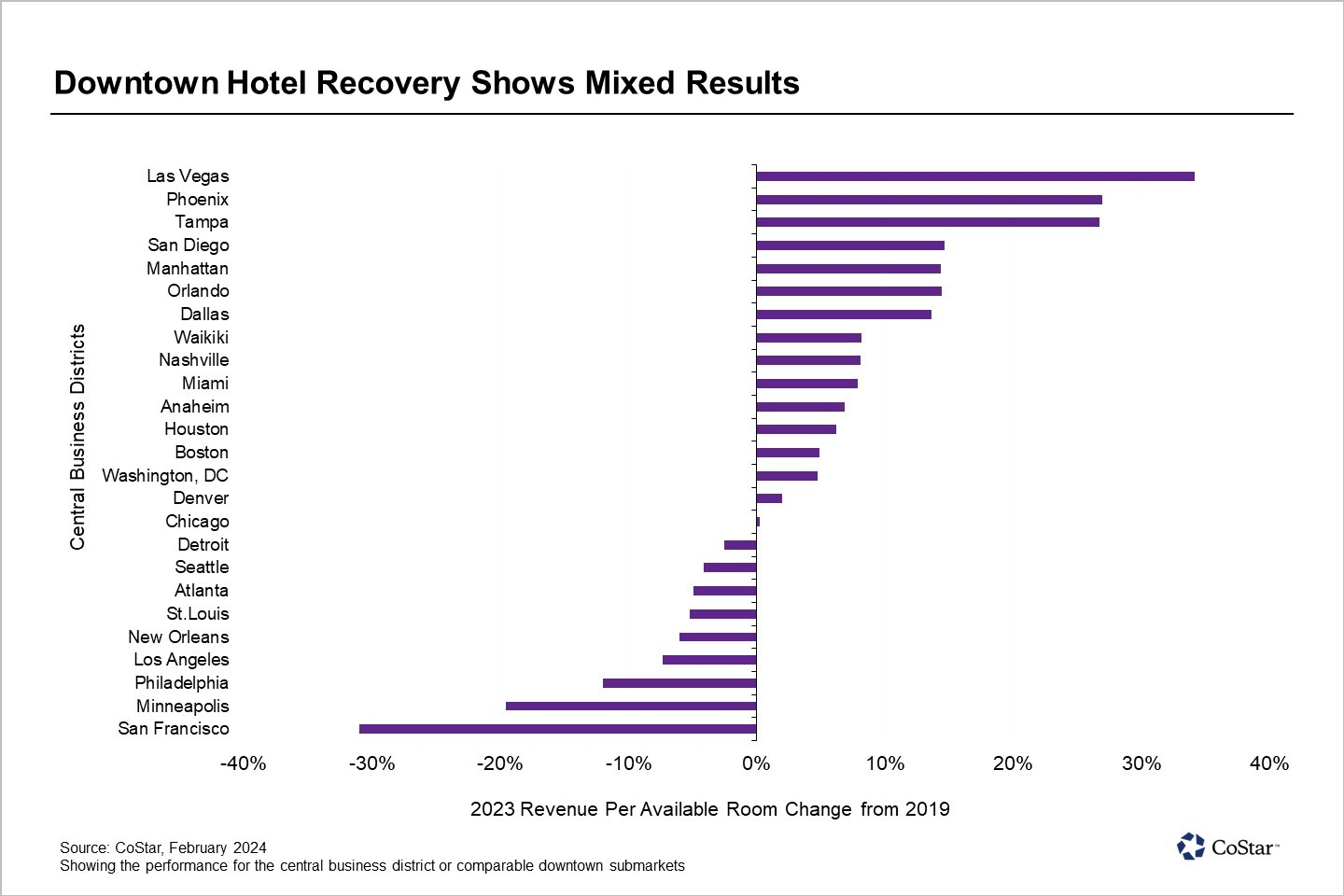

📈 CHART OF THE DAY

The return of workers to downtown offices in 2023 benefitted many hotels in central business districts, but unevenly. Cities like San Francisco, Minneapolis, and Philly saw significant revenue drops of up to 30% compared to 2019, while Las Vegas, Phoenix, and Tampa were on the other end of the spectrum, enjoying up to 35% higher revenue per available room.

What did you think of today’s newsletter? |