Warehousing Demand Falls as Retailers Trim Inventories

Plus: Yardi Matrix challenges the optimistic projections of a rapid decrease in the U.S.’s apartment oversupply.

Jordan B. & Han-Gwon Lung

February 15, 2024

Together with

Good morning. The U.S. warehousing sector is contracting as companies upgrade or consolidate storage sites rather than add new ones. Meanwhile, contrary to predictions by some experts, the U.S. apartment oversupply will not decline by EOY 2024.

Today’s issue is brought to you by Matheson Capital.

Market Snapshot

|

|

||||

|

|

*Data as of 2/14/2024 market close.

LOGISTICS REPORT

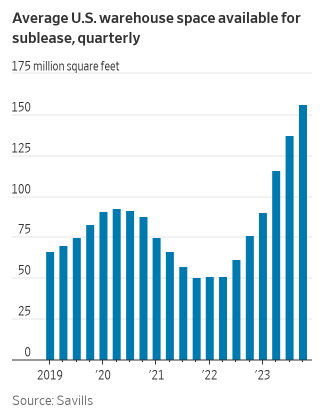

Subleases Surge as US Warehousing Demand Shrinks

The once-booming U.S. warehousing sector is now contracting with companies consolidating and upgrading warehouses instead of adding new ones.

Around the country: Retailers are reducing inventories and realigning supply chains for pre-pandemic stocking and consumer spending patterns. Companies like Newell Brands, Rite Aid, and Fanatics are closing or upgrading existing facilities. And the amount of U.S. warehouse space listed for sublease reached a record high of over 156MSF in 4Q23, more than 3x what was available in 4Q21.

Rental impact: Exploding demand and low vacancy rates during the pandemic led to a nearly 24% increase in the average warehouse asking rent in 2022 compared to a 6.3% annual increase in 2019. However, the rent growth has since slowed, rising 12.5% in 2023, according to JLL.

Shifting inventory: The “just-in-case” inventory management strategy adopted during the pandemic due to supply chain snarls is being replaced by the “just-in-time” lean inventory approach. Companies are subleasing excess space they added based on projections that didn’t materialize. This adjustment reflects a return to more moderate growth in consumer spending and supply chain projections.

➥ THE TAKEAWAY

A dawn of a new era: Emerging trends in U.S. warehousing indicate a shift towards consolidation and upgrades rather than expansion. Companies are streamlining operations by consolidating warehouses, upgrading to more efficient facilities, and integrating automation and digitization. This adjustment aligns with a return to lean inventory management strategies and more realistic consumer spending projections.

SPONSORED BY Matheson Capital

Proven Value-Add Multifamily Investment Opportunity

Matheson Capital is thrilled to present its latest investment offering, Residences at St. George, a 248-unit multifamily community located in Savannah, GA. Here’s why they are excited about this opportunity:

-

Assumption of a 2.95% fixed-rate loan with 8+ years remaining on its term.

-

Acquisition price of $156,000 per unit, which is below the comparable sales from Q4 2023.

-

A proven value-add upside that offers a clear path for NOI growth.

-

The strong population and employment growth currently being experienced in Savannah, GA.

Based in Charleston, SC, Matheson Capital specializes in Southeastern US real estate, with a proven track record of 15 acquisitions and seven exits since 2018 with an average LP IRR of 40%**.

*See the sponsor’s disclosures at the boom on the newsletter.

✍️ Editor’s Picks

-

What’s next: Investment sales broker Bob Knakal, responsible for deals worth $22B, was unexpectedly dismissed from JLL after six years, coinciding with a New York Times story.

-

Refinancing wave: In 2024, the amount of CRE debt maturing shot up from $659B to $929B due to loan extensions and modifications.

-

Fortune favors the rich: PE firm TPG, armed with $51B, remains optimistic about opportunities in credit, infrastructure, and real estate.

-

Shadowy showdown: U.S. banks loaned over $1T to shadow banks last year, despite regulator concerns, according to the Federal Reserve.

-

Rates ascend: The 30-year mortgage rate reached 6.87%, its highest level in 2 months, potentially slowing housing recovery.

-

Sliding sale: Tishman Realty will sell the 1,218-room Sheraton Grand Chicago Riverwalk hotel to Marriott (MAR) for $500M this year, exercising an option from a 2017 settlement.

-

Deal of the day: Welltower (WELL) forms a strategic partnership with Affinity Living Communities, acquiring a portfolio of 25 active adult communities for $969M.

-

The Two Towers: Commercial and multifamily mortgage loan originations dropped 25% YoY in Q4, with decreases in office, healthcare, multifamily, and industrial. Meanwhile, retail and hotel originations went up 50% and 81%.

-

Solar-powered: Solar use on U.S. farms is up 30% in the past five years, with nearly 117K farms in 2022 compared to a little over 90K in 2017, while wind turbine installation grew just 2.7%.

🏘️ MULTIFAMILY

-

Rent sinks, banks shrink: Rent laws leading to declining apartment values in NYC squeezed lender NYCB with $18B in loans at risk.

-

Sizzling development: Lakewood-based developer Schwartz purchased a 1.3-acre site in Jersey City’s West Side neighborhood for $12.5M, planning to build 365 apartments.

-

Transforming Little River: Swerdlow Group submitted a $2.6B proposal to Miami-Dade County to transform a section of the city with big-box stores, a new Tri-Rail station, and nearly 5K affordable and workforce apartments.

-

Mixed results: Airbnb (ABNB) beats revenue forecasts with $2.22B but reports a $349M loss. The Uber for vacation rentals plans to expand into under-penetrated markets this year.

-

Built-to-Rent boom: A $3B wave of built-to-rent housing investment highlights continued demand as high mortgage payments deter potential homeowners.

🏬 RETAIL

-

Bowling to expansion: Playa Bowls, which serves acai, pitaya, mango, and coconut bowls, is expanding its chain rapidly, aiming to double its national footprint.

-

Shaming Uncle Sam: NYCHA officials ignored corruption warnings, leading to the largest single-day federal bribery takedown in DOJ history ($2M kickbacks).

-

Bankruptcy blues: Boston Market owner, Jignesh “Jay” Pandya, and his wife declared personal bankruptcy in Pennsylvania after a $15M judgment was awarded to US Foods.

🏢 OFFICE

-

Camps divided: Morgan Stanley (MS) predicts a 30% drop in U.S. office valuations, with a 20% drop already behind us.

-

Futuristic starbase: SpaceX plans a $100M, five-level office in Brownsville, Texas for its Starship rocket development and production facility.

-

Retail rises: Retail is still seen as a rare bright spot in the bleak CRE market, as Facebook’s parent company (META) shrinks its NYC office footprint.

-

Making moves: CoStar Group (CSGP) is relocating its global HQ from D.C. to Northern Virginia, investing $20M and creating 150 new jobs.

MULTIFAMILY OUTLOOK

Apartment Oversupply Persists Despite Decline Predictions

In a recent analysis, Yardi Matrix challenges the optimistic projections of a rapid decrease in the U.S.’s apartment oversupply, predicting a sustained period of elevated apartment deliveries until 2026.

Too much of a good thing: A whopping 766,353 units are scheduled for completion by early 2026, marking a significant quarterly and annual increase. Additionally, the first quarter of 2024 saw 483,207 units in the lease-up phase, contributing to a total of 1.25 million units in the pipeline. Yardi attributes these numbers to extended construction times for various property types, with garden and midsize properties experiencing near-record construction durations.

Signs of a slowdown: Despite the robust pipeline, Yardi foresees a “gradual but not disastrous slowdown” in multifamily development, expecting the new supply to bottom out in 2026. The analysis is supported by data from the Census Bureau and indicators like the Architectural Billing Index, which has shown consistent billing contraction. Interestingly, certain metros have already begun to see a decline in new apartment supply, with significant drops in cities like Indianapolis, Salt Lake City, and Seattle.

➥ THE TAKEAWAY

The road ahead: Yardi’s forecast involves a mild recession in 2024, followed by a recovery starting in 2027. However, this recovery is modest, with new supply anticipated to reach about 377,000 units in 2026, gradually increasing in the subsequent years. This forecast hinges on several factors, including economic conditions and financing. In a less optimistic scenario, Yardi predicts a deeper recession and a substantial decrease in new construction starts, leading to a 38% reduction in new supply.

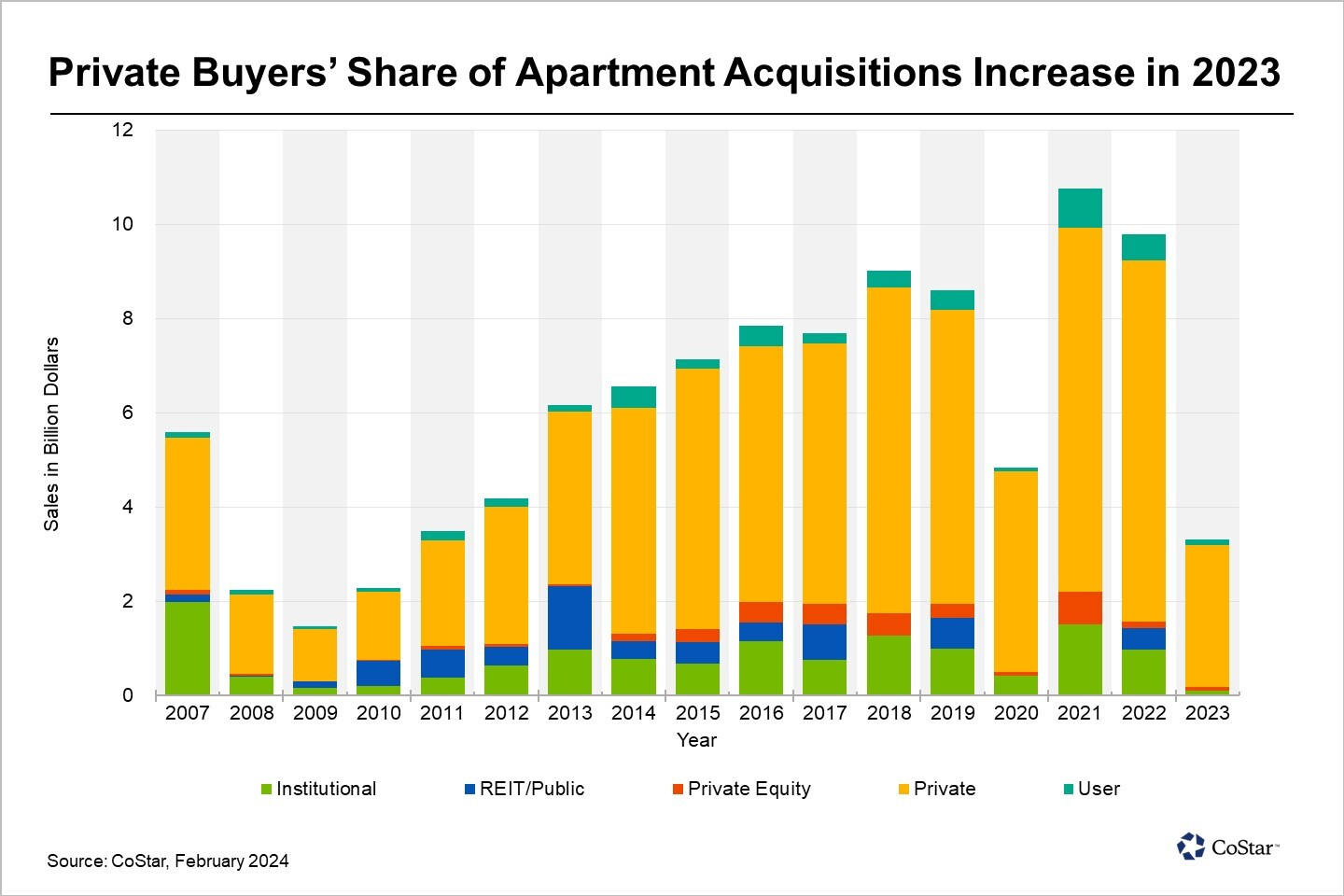

📈 CHART OF THE DAY

Historically, private buyers have dominated the LA multifamily market. But in recent years, their piece of the pie has gotten bigger than ever, both in terms of absolute dollar figures and relative to other types of buyers.

What did you think of today’s newsletter? |

* Financial metrics are projections and/or forward-looking statements, and not guarantees of profit. See risk factors and disclosures in Private Placement Memorandum for more details.

**LP IRR is based on the weighted average of seven realized sales.